Without any deliberate purpose, the insured might have 2 (two) fire insurance policies from 2 (two) insurance companies. A first policy issued by X Insurance Co. and another one issued by Y Insurance Co.

Let’s say that the trade of the insured’s business is a retailer of electronics goods, like television, air conditioner, refrigerator, etc.

The sum insured for each policy above might be as follows :

| Insurance Co. | Sum Insured on Building | Sum Insured on Stock-in-Trade |

|---|---|---|

| X | 20,000.00 USD | 4,000.00 USD |

| Y | 10,000.00 USD | 6,000.00 USD |

One day, the building was on fire. Based on the spot investigation, loss adjuster reported that the cause of loss was due to fire following a short circuit. The insured, then, propose a claim as much as USD 20,000.00 on building loss and USD 3,000.00 on stock-in-trade loss. The value of USD 20,000.00 was considered by damaged building after the loss which was not stable anymore and needs to be rebuilt after the fire damage. Let’s say, the building was built in 2012 and loss damage happens in 2017. Meanwhile, the stock-in-trade is a new item. So, how we can calculate the actual loss and respective liability for each insurance company?

Claim Settlement Using “Sum Insured” Method

A. On Building

First, we need information about construction index based on local price. In Indonesia, we can find such index from the Local Construction Guidance Book issued by National Planning Board and Finance Department. Second, we calculate the sound value of the respective items. If it assumed that for 100 m2 loss of building need cost USD 100.00/m2, so the rebuilt cost of the building is 100 m2 x USD 100.00/m2. Depreciation value is assumed by 10% for 5 year period. Then, the sound value of building is 100 m2 x USD 100.00/m2 – (10% x 100 x 100) = USD 9,000.00. This value is lower than proposed value by the insured because the insured made a claim without considering adjusted construction index and yearly depreciation.

Then, the claim payment on building received by the insured is USD 6,000.00 + USD 3,000.00 = USD 9,000.00.

B. On Stock-in-Trade

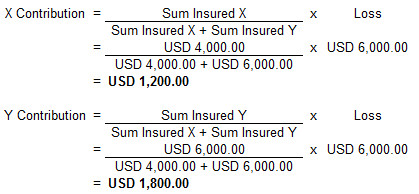

For the loss of electronic goods as stock-in-trade, we need information on the stock declaration in every month and compared with damaged items found while taking a claim investigation. If the item is a new condition, no depreciation will be made. And with an assumption that the actual loss for stock-in-trade is same with the proposed value by the insured (USD 6,000.00), we can calculate loss based on the formula below :

Stock-in-trade claim settlement using “sum insured” method :

Then, the claim payment on stock-in-trade received by the insured is USD 1,200.00 + USD 1,800.00 = USD 3,000.00.

So, the compensation paid by X Insurance Co. is USD 6,000.00 + USD 1,200.00 = USD 7,200.00, and in other side, Y Insurance Co. will pay the insured in a value of USD 3,000.00 + USD 1,800.00 = USD 4,800.00. Total claim payment received by the insured is USD 7,200.00 + USD 4,800.00 = USD 12,000.00.